2026 Home Insurance Audits: Why Older Eastside Homes are Being Flagged

2026 Home Insurance Audits: Why Older Eastside Homes are Being Flagged

A neighbor of mine recently reached out, frustrated and a bit blindsided. Their story is one that should be a wake-up call for every homeowner on the Eastside. They’ve lived in their home for over 40 years, have a spotless claim history, and have stayed with the same insurer for decades.

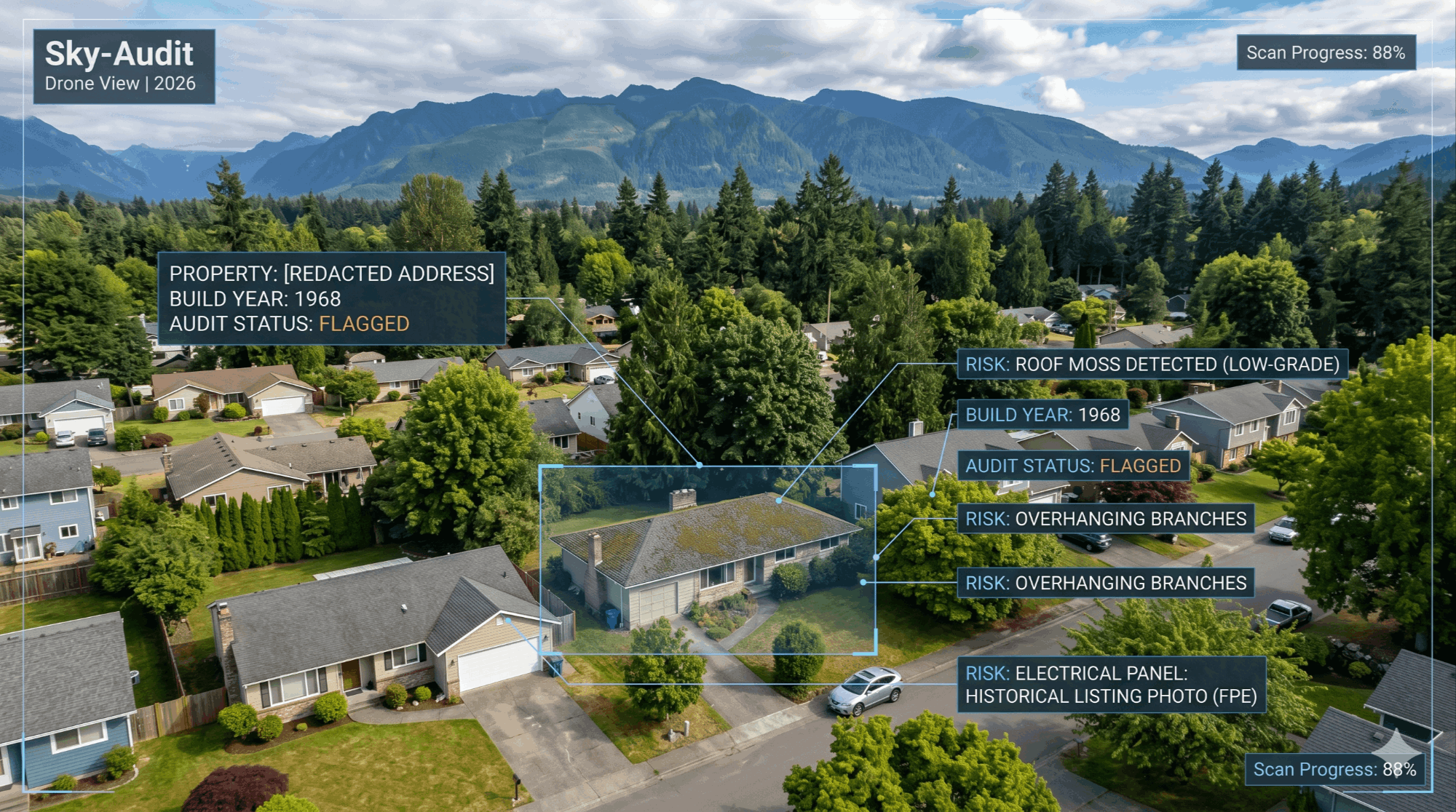

Recently, they received a letter that didn't just thank them for their loyalty. Instead, it was a request: send high-resolution photos of the roof and property, or the insurer would send out an inspector to walk the perimeter. They chose the inspection. The result? Despite their decades of loyalty, the insurer flagged their 1968-built home and gave them until August to perform specific maintenance—primarily "blowing off" a 7-year-old roof that had accumulated moss and getting a professional electrical audit.

I thought you should know: the way insurance companies "see" your home has fundamentally changed. In 2026, the traditional physical inspection is being replaced by high-resolution "Sky-Audits." If you own an older home on the Eastside—whether it’s a mid-century gem in Bellevue or a wooded retreat in Woodinville—you are likely already under the digital microscope.

The Rise of Digital Surveillance in Risk Management

It’s not just your imagination; the insurance industry is tightening its belt. National data from early 2026 shows that homeowners insurance premiums have surged significantly, with the average U.S. policy now hovering near $3,000. While Washington state has historically enjoyed more stable rates than the hurricane-prone South, our local carriers are now using sophisticated tools to justify price hikes and cancellations.

But the bigger story is the cancellations. Since 2021, insurers have canceled at least 1.4 million policies nationwide as they aggressively "trim their books" to manage risk. In 2026, insurers are moving away from broad regional data and toward hyper-local ZIP code modeling. They are using satellites and AI to identify specific houses—not just neighborhoods—that they deem "uninsurable."

The View from the "Prop-Tech" Inside

To be sure, this technology isn't a mystery to me. When I was working in a Prop-Tech startup from 2021 through 2023, our team was developing these exact Advanced AI models. We were training algorithms to analyze the physical attributes of homes using listing data, Google Street View, and high-res satellite imagery to help underwriters understand risk without ever leaving their desks. What was "cutting-edge" then is now the standard operating procedure for insurance companies.

What Triggers an Audit?

Insurers aren't just looking for fire hazards; they are looking for "attritional risk"—the small things that suggest a lack of maintenance. Common triggers for a 2026 audit include:

- The Roof Profile: AI can now detect moss growth, missing shingles, or aging materials from space. On the Eastside, our damp climate makes moss a primary target for "risk" flags. Even a relatively young roof can be flagged if it hasn't been maintained.

- Yard Debris & Overhanging Limbs: If your property has heavy branches scraping the roofline or significant debris in the yard, it’s a red flag for potential liability and property damage.

- Historical Listing Data: Insurers are scraping old listing photos and marketing descriptions. If a 2018 listing photo shows a Federal Pacific Electric (FPE) or Zinsco panel, they may flag the home for a mandatory electrical audit or upgrade before renewing, as these panels are notorious for failing to trip and causing fires.

How to Stay Below the Radar

The Washington State Office of the Insurance Commissioner issued a data call in April 2026 to track these non-renewals, but you shouldn't wait for a letter to arrive. Here is how to protect your coverage:

- Maintain the "Envelope": Keep your roof clean and gutters clear. A "mossy" roof is a top trigger for a Sky-Audit flag.

- Trim the Canopy: Ensure no branches are overhanging or touching the roofline.

- Proactive Electrical Checks: If you have a 1960s-era home, have a licensed electrician look at your panel before the insurer asks for a report.

If you’ve received a request for photos or an "inspection notice" from your insurance company, DON’T IGNORE IT.

- Request the Specifics: Ask the insurer exactly which component is being audited.

- The "Pre-Audit" Cleanup: Believe it or not, cleaning up the exterior can sometimes de-escalate the insurer’s "risk" perception.

- Shop the "Independent" Market: If your insurer drops you, take a look at independent brokers who have access to "secondary" markets that specialize in older homes, though the premiums will likely be higher.

Integrity First: Practical Next Steps

Navigating these new insurance hurdles can feel overwhelming, especially when you’ve done everything right for years. If you’re unsure how to handle a request from your insurer or need a recommendation for a reliable local trade to help with a "pre-audit" cleanup, let’s chat. I’m here to offer a practical perspective on your next steps and help you protect the value of your home without the high-pressure sales pitch.

About Kurt Kreager: A Greater Seattle Eastside authority since 2013, Kurt is a Managing Broker and former licensed contractor who views real estate through the lens of integrity and long-term value. From "Backyard Goldmines" (DADUs) to navigating complex 2026 housing laws, Kurt prioritizes serving people over chasing the next dollar.

Categories

Recent Posts

GET MORE INFORMATION